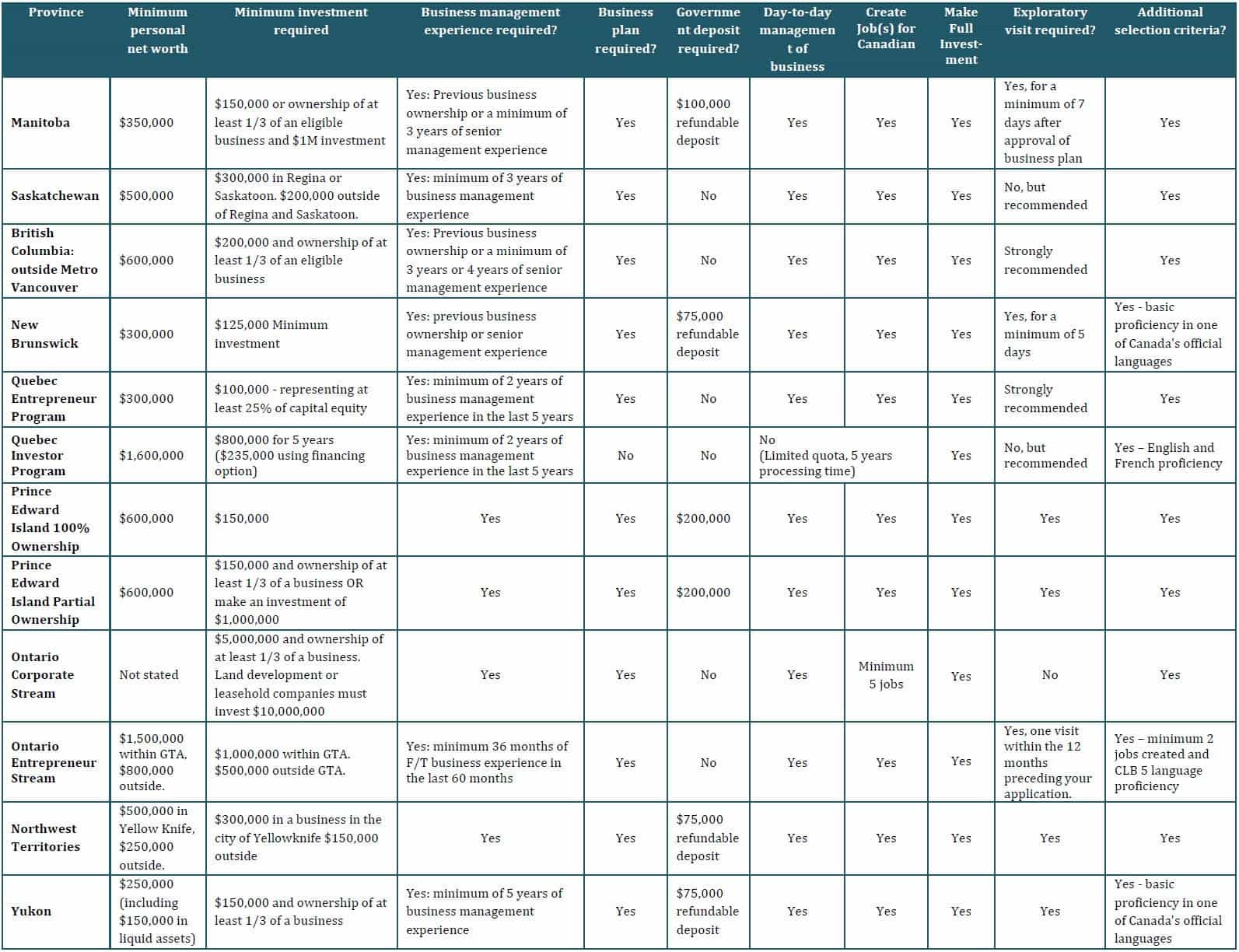

Understanding the First Home Savings Account (FHSA) for New Canadians

Thinking about buying your first home in Canada? As a newcomer, saving for a down payment may take time. To support this goal, Canada’s federal government has a registered savings plan known as the First Home Savings Account (FHSA).

If you’re eligible, this special savings account may help make it easier to set money aside for your future home.

Learn more about TD New to Canada Banking Package

Read on to find helpful information to better understand the FHSA, what it is, how it works, and how it may fit into your home ownership goals as a newcomer.

Here’s what we’ll cover:

Eligibility – Who can open an FHSA and when

FHSA basics – What it is and how it works

Why consider TD – A few reasons newcomers may choose TD for their FHSA

FHSA vs. other plans – How it compares to a Tax-Free Savings Account (TFSA) or Registered Retirement Savings Plan (RRSP)

Getting started – Opening an FHSA and choosing the right account for you

FHSA Basics: What it is and how it works

The First Home Savings Account (FHSA) is a registered savings plan introduced by the Canadian federal government in 2022. It is designed to help eligible Canadian residents, including newcomers, save for their first home in Canada.

You can contribute up to $8,000 per year, with a lifetime limit of $40,000. Contributions towards your FHSA may be tax-deductible. Any savings and investment growth in the account can be withdrawn tax-free when used to buy a qualifying first home.

Ready to bank? Learn more about TD New to Canada Banking Package today

Why Consider TD – A Few Reasons Newcomers May Choose TD for Their FHSA

As a newcomer settling into life in Canada, finding the right financial institution can help make a meaningful difference, especially when planning for something as important as your first home. Here are a few ways TD may support you on that journey with an FHSA:

✔ Plan your mortgage with greater clarity

While tools like the TD Mortgage Affordability Calculator can help you plan for your mortgage and down payment, an FHSA from TD can help you save for the same. This may make it easier to select the right amount and type of mortgage based on your income, expenses, and long-term goals.

✔ Get financial advice tailored to your needs

At TD, we’re here to support newcomers in building a strong financial future. You can book a Goal Builder appointment with a personal banker to understand what steps and products may help get you closer to your home ownership goals. It’s about guidance that fits your unique situation.

✔ Choose from flexible investment options

With a TD investment services FHSA, you’re not limited to just saving in cash. You can choose from a variety of investment options that go into an FHSA, such as GICs (Guaranteed Investment Certificates) and mutual funds. This flexibility may help you grow your savings over time while staying within an account designed for your first home.

FHSA vs. Other Plans: How it compares to a Tax-Free Savings Account (TFSA) or Registered Retirement Savings Plan (RRSP)

If you’re thinking about saving for a first home, it may help to understand how the First Home Savings Account (FHSA) compares to other registered plans available in Canada. Here’s how it compares against two common options:

✔ RRSP vs. FHSA

A Registered Retirement Savings Plan (RRSP) is mostly used for saving for retirement. However, it may also help with buying your first home through the Home Buyers’ Plan (HBP).[1] You can withdraw up to $60,000 toward a home purchase, but you’ll need to repay that amount. The repayment period begins the second year after the withdrawal, and you have up to 15 years to repay the full amount.

However, with an FHSA, withdrawals for a qualifying first home purchase—along with any investment earnings—are not taxed and do not need to be repaid.

✔ TFSA vs. FHSA

A Tax-Free Savings Account (TFSA) allows you the flexibility to save for a multitude of short and long-term financial goals. You can withdraw qualifying funds from the TFSA without paying tax. This can make the TFSA a great tool to save for big-ticket items, like purchasing a home.

The FHSA is designed to support First-Time Homebuyers with useful features from both plans, offering tax-deductible contributions and tax-free withdrawals when used for a qualifying purchase. [2]

Learn more about TD New to Canada Banking Package

Getting Started: Opening an FHSA and Choosing the Right Account for You

To open a First Home Savings Account (FHSA), you’ll first want to speak with your bank or personal banker. You’ll need to provide some basic documentation, such as valid identification, your Social Insurance Number (SIN), proof of Canadian residency, and a completed application. Once your account is open, you can begin contributing toward your first home purchase.[3]

There are a few types of FHSAs that TD has to offer, depending on how you’d like to manage your funds:

Multi-Holding Account- Holds your funds in cash, GICs or Mutual Funds all within one account.

Direct Investing Account- A self-directed investing option with access to a wider range of investments, such as mutual funds, stocks, GICs and Bonds.

Each type of plan has different features, so it’s helpful to talk with a TD personal banker to find the option that suits your needs and comfort level.

Eligibility: Who Can Open an FHSA and When?

To open a First Home Savings Account (FHSA), you must meet a few conditions set by the Canada Revenue Agency (CRA). This includes:

A Canadian resident

18 years or older[4]

Have a valid Social Insurance Number (SIN)

A first-time home buyer[5]

For newcomers to Canada, the FHSA may be a helpful way to begin saving for a first home. It offers tax advantages and the flexibility to invest your contributions. Once you’re eligible and feel ready, opening an FHSA could be a simple step toward reaching your homeownership goals.

Ready to bank? Learn more about TD New to Canada Banking Package today

Over 150 years helping Canadians:

TD has a proud history of delivering financial solutions to Canadians for more than 150 years.

TD also brings a century of experience helping newcomers navigate the unique challenges of the Canadian banking system.

With over a thousand branches, and the ability to also serve you in more than 80 different languages, TD has become one of the largest and most trusted banks in Canada, now serving 16 million Canadians.

TD offers online support and resources of interest to newcomers on topics such as banking basics, moving to Canada, credit score essentials, and more. TD is open longer hours for your convenience and has thousands of ATMs across Canada to help you take care of your everyday banking needs quickly and easily.

Ready to Bank?

Learn more about TD New to Canada Banking Package today.

Book an appointment to talk with a TD Personal Banking Associate about the TD New to Canada Banking Package. You can book online right away or visit the TD website to learn more.

Legal Disclaimer:

Information provided by TD Bank Group and other sources in this article is believed to be accurate and reliable when placed on this site, but we cannot guarantee it is accurate or complete or current at all times. The information in this article is for informational purposes only and is not intended to provide financial, legal, accounting or tax advice, and should not be relied upon in that regard. This information is not to be construed as a solicitation to buy. Products and services of the TD Bank Group are only offered in jurisdictions where they may be lawfully offered for sale. All products and services are subject to the terms of the applicable agreement. The information in this article is subject to change without notice.

® The TD logo and other TD trademarks are the property of The Toronto-Dominion Bank or its subsidiaries.

[1] Certain conditions must be met in order to be eligible to participate in the HBP, including the following: you must be considered a first-time home buyer; you must have a written agreement to buy or build a qualifying home, either for yourself or for a related person with a disability; you must be a resident of Canada when you withdraw funds from your RRSPs under the HBP and up to the time a qualifying home is bought or built; you must intend to occupy the qualifying home as your principal place of residence within one year after buying or building it. If you help a related person with a disability to buy or build a qualifying home, you must intend that the related person with a disability occupies the qualifying home as their principal place of residence. In all cases, if you have previously participated in the HBP, you may be able to do so again if your repayable HBP balance on January 1st of the year of the withdrawal is zero and you meet all the other HBP eligibility conditions.

[2] Canada Revenue Agency, First Home Savings Account (FHSA), Government of Canada, 2025, https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/first-home-savings-account.html, (accessed 8 July 2025).

[3] Government of Canada, Opening, closing and FHSA, Canada Revenue Agency, https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/first-home-savings-account/opening-closing-and-fhsa.html (accessed 8 July 2025).

[4] In certain provinces and territories, the legal age at which an individual can enter into a contract including opening a FHSA is 19. You must be at the age of majority in your province of residence and provide a valid Social Insurance Number (SIN). FHSA cannot be opened after the end of the year you turn 71.

[5] An individual is considered to be a first-time home buyer if at any time in the part of the calendar year before the account is opened or at any time in the preceding four years they did not live in a qualifying home (or what would be a qualifying home if located in Canada) that either (i) they owned or (ii) their spouse or common-law partner owned (if they have a spouse or common-law partner at the time the account is opened).